The $16B Recovery: Why Consumer VC Just Had Its Best Quarter Since 2021 (And What’s Actually Changed)

So after four years of “consumer is dead” think pieces and founders pivoting to B2B SaaS to get funded, something quietly shifted in Q1 2026.

$16 billion in fresh consumer VC commitments are deploying right now.

Six major consumer funds closed in the last 90 days (vs. zero in Q1 2025).

$3B+ in consumer M&A closed in January-February alone—including Poppi ($1.95B to PepsiCo), Dr. Squatch (~$1.5B to Unilever), Siete Foods (~$1.2B to PepsiCo), and Rhode ($1B to e.l.f. Beauty).

For context: In Q1 2025, consumer VC deployed only $800M—a six-year low. Deal activity was dead. Major funds weren’t raising. The entire category was written off.

One year later, deployment is up 20x.

But here’s what everyone’s missing: This isn’t 2021 coming back. The rules have completely changed.

The platform VCs (Forerunner, VMG, L Catterton) raised $14B+ in the last 15 months and they’re not deploying into DTC brands burning $10M/year on Facebook ads hoping to sell for 20x revenue.

They’re deploying into:

GLP-1 nutrition brands (23% of US households now have a GLP-1 user)

Functional beverages with actual retail traction (prebiotic sodas up from $33M to $777M in 3 years)

Prestige beauty at 14.9x EBITDA multiples (vs. 9.8x for mass consumer)

Wellness tech that’s capital-efficient from day one

Consumer VC is back. But it’s a completely different game.

Let me show you what actually changed, who’s winning in the new era, and why the next 12 months will determine if this is a real recovery or another false start.

The Numbers That Show This Isn’t a Mirage

Let’s start with the data that proves something fundamental shifted:

Q1 2025 vs. Q1 2026 (One Year Apart):

Q1 2025 (The Bottom):

VC deployed: $800M (6-year low)

Total deals: 111

Major consumer fund closes: 0

Macro context: “Tariff shock, deep uncertainty in CPG”

Q1 2026 (The Recovery):

Fresh commitments deploying: $16B

M&A (Jan-Feb alone): $3B+

Major funds closed (last 90 days): 6 of 10 largest consumer funds

GP sentiment: “Cautiously offensive” (no longer defensive)

For perspective: $16B in fresh commitments is:

2.4x the total US consumer VC deployed in all of 2024 ($6.8B)

20x Q1 2025 deployment ($800M)

Close to 2021 levels (but structured completely differently)

This isn’t a small uptick. This is a category coming back from the dead.

The Six Fund Closes That Changed Everything

Between November 2024 and March 2026, six major consumer-focused funds closed with a combined ~$16B in commitments.

Here’s the breakdown:

1. L Catterton (May 2025): ~$11B

Largest consumer-focused PE firm globally

Strategy: Large-scale buyouts + growth equity

Status: Largest consumer fund close in history

Why this matters:

L Catterton isn’t a seed fund betting on DTC startups. They’re writing $100M-500M checks into profitable, scaled brands.

Recent L Catterton investments:

Birkenstock (took public, $8B valuation)

Glossier (growth equity round)

Savage X Fenty (Rihanna’s lingerie brand)

When the world’s largest consumer PE fund raises $11B, it’s a signal: Institutional capital believes in consumer again.

2. VMG Partners Consumer VI (May 2025): $1.0B

At hard cap (fully subscribed)

Focus: Growth-stage consumer brands ($50-200M revenue)

Strategy: Operational value-add, not just capital

VMG’s track record:

Olipop (prebiotic soda, now $500M+ revenue)

Graza (olive oil, premium positioning)

Liquid Death (acquired by Keurig Dr Pepper for $1.4B, 2024)

VMG raised at hard cap = LPs are oversubscribing because returns have been strong.

3. Forerunner Ventures VII (May 2025): $1.0B

At hard cap (oversubscribed)

Focus: Early-stage consumer brands + platforms

Led by Kirsten Green (legendary consumer investor)

Forerunner’s portfolio:

Glossier (early investor)

Chime (fintech, but consumer-facing)

Faire (wholesale marketplace)

Forerunner’s thesis: Consumer brands that own distribution or have platform economics (not just DTC brands hoping for acquisition).

4. Prelude Growth Partners III (Aug 2025): $600M

2.4x larger than prior fund (Fund II was $250M)

Focus: Growth-stage beauty, wellness, food

Why fund size matters:

When a fund raises 2.4x more than its previous fund, it means:

Fund II returns were exceptional (LPs reinvesting)

Fund III can write bigger checks (moving upmarket)

Investor confidence is back

5. Bansk Group Fund II (Dec 2025): $1.45B

45% above $1B target

Focus: Consumer brands, healthcare, financial services

Strategy: Operational transformation, not passive capital

Raising 45% above target = LPs fighting to get allocation.

6. Encore Consumer Capital V (Jan 2026): $350M

Oversubscribed

Focus: Emerging consumer brands, sustainability-focused

Plus additional closes (Jan-Mar 2026):

CAVU Consumer Partners V: $325M (18% above target)

SEMCAP Food & Nutrition: $125M

Coefficient Capital + Apex: $530M

Cutting Horse Fund: $75M

Combined total: ~$16B in the last 15 months.

For context: In 2022-2024 (3 years), consumer funds raised ~$8B total.

In the last 15 months, they raised 2x that amount.

The capital drought is over.

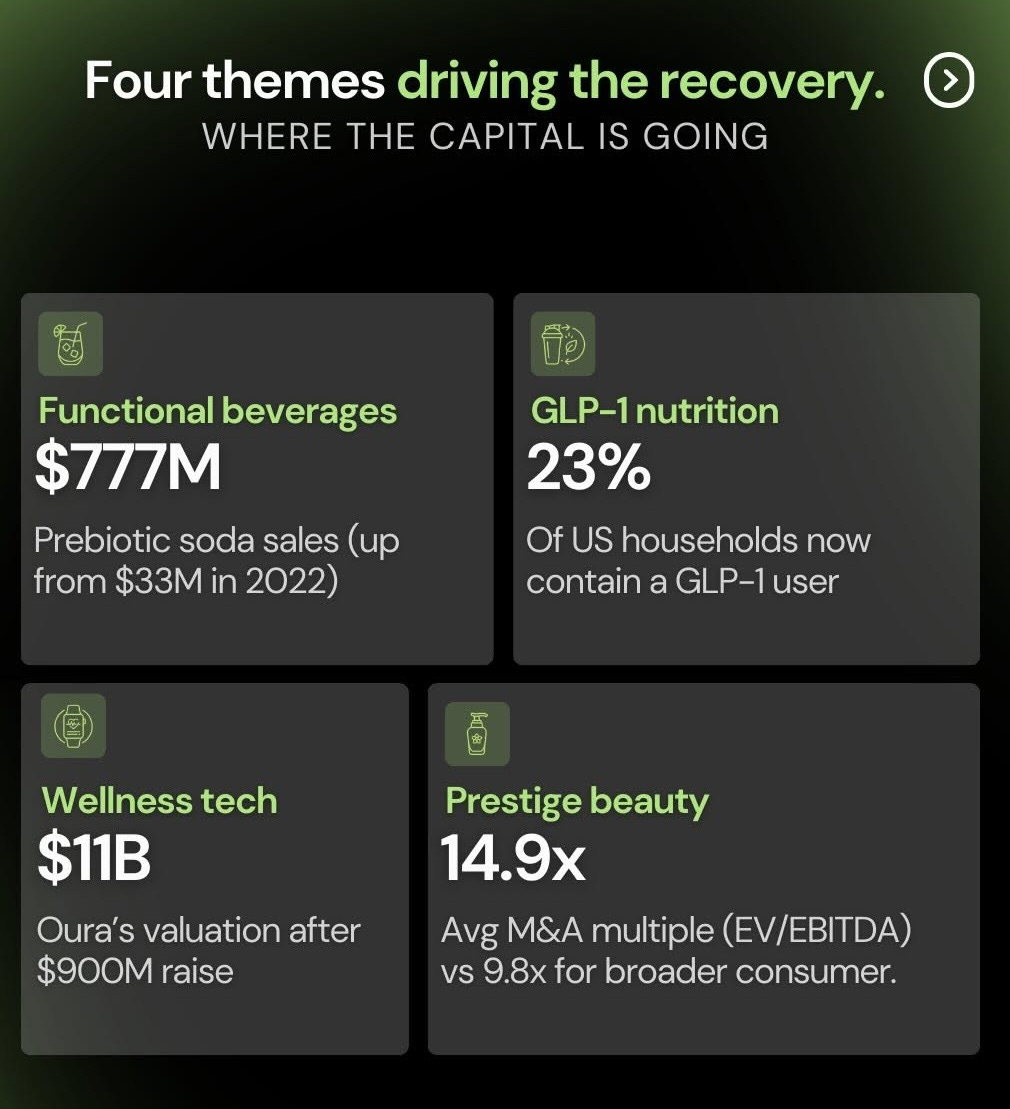

What Actually Changed: The Four Investment Themes Driving Deployment

Consumer VC isn’t back because investors suddenly forgot about 2022-2024 losses.

It’s back because four specific categories are working—and the data proves it:

Theme 1: Functional Beverages ($777M in Prebiotic Soda Alone)

The data:

2022 prebiotic soda sales: $33M

2025 prebiotic soda sales: $777M

Growth: 23.5x in 3 years

Category leaders:

Poppi: Acquired by PepsiCo for $1.95B (Jan 2026)

Olipop: ~$500M revenue, growing 100%+ annually

Culture Pop: Emerging player, VMG-backed

Why this category works:

Consumer demand:

Functional benefits (gut health, digestion)

Better-for-you (low sugar, natural ingredients)

Tastes good (not medicinal like Kombucha)

Unit economics:

Gross margins: 55-65% (strong for beverage)

Repeat rate: 40-50% (high for soda category)

CAC: $15-25 (social + retail sampling)

LTV: $120-180 (6-12 month retention)

LTV/CAC: 5-9x (venture-backable)

Investor returns:

CAVU invested in Poppi early (estimated $5M at $50M valuation)

Exit: $1.95B to PepsiCo

Return: ~88x in ~4 years

This is why VCs are back in beverages. When one fund returns 88x, every fund wants the next Poppi.

Theme 2: GLP-1 Nutrition (23% of US Households)

The data:

15M+ Americans on GLP-1 drugs (Ozempic, Wegovy, Mounjaro, Zepbound)

23% of US households contain a GLP-1 user

Market size: GLP-1 users need 1,800-2,200 calories/day vs. 2,000-2,500 for non-users

Opportunity: High-protein, nutrient-dense foods for smaller appetites

What’s getting funded:

Nutrition brands solving for:

High protein per calorie (20g+ protein in 200-300 calories)

Nutrient density (vitamins, minerals in small portions)

Easy digestion (GLP-1 users have slower gastric emptying)

Portion control (single-serve, 200-400 calorie meals)

Examples:

Ample: Meal replacement shakes, high-protein

Magic Spoon: High-protein cereal (20g protein per serving)

Huel: Complete nutrition, 400 calories per serving

Why VCs care:

Addressable market:

15M GLP-1 users today

Projected 30M by 2028

Average spend: $200-300/month on specialized food

TAM: $6-9B annually

Unit economics:

High AOV ($50-80 per order, subscription-based)

High retention (medical need, not discretionary)

LTV: $1,200-1,800 (12-18 month average subscription)

This is a structural tailwind. As long as GLP-1 adoption grows, these brands grow.

Theme 3: Wellness Tech ($11B Valuations, Capital-Efficient)

The standout: Oura Ring

Oura’s metrics:

Revenue: ~$500M (2024, estimated)

Recent raise: $900M at $11B post-money valuation (2025)

Multiple: 22x revenue

Why Oura commands premium valuation:

1. Hardware + software moat:

Ring hardware: $299-399 (one-time purchase)

Membership: $5.99/month (recurring revenue)

Blended model: Hardware at cost, profit from subscription

2. Retention economics:

Membership retention: 80%+ annually

Once you buy the ring, you keep subscribing

3. Data moat:

Millions of users contributing sleep/health data

Proprietary algorithms improving with scale

Network effects in health tracking

Comparison to traditional consumer:

Traditional DTC brand:

Hardware-only (one-time purchase)

No recurring revenue

Valuation: 2-4x revenue

Oura:

Hardware + subscription

Recurring revenue = 60%+ of total

Valuation: 22x revenue

VCs want consumer businesses with SaaS economics. Oura proved it’s possible.

Theme 4: Prestige Beauty (14.9x EBITDA vs. 9.8x Mass Consumer)

The data:

Prestige beauty M&A multiple: 14.9x EBITDA (average)

Broader consumer M&A multiple: 9.8x EBITDA

Premium: 52% higher multiples for prestige beauty

Recent prestige beauty exits:

Rhode (Hailey Bieber):

Acquired by e.l.f. Beauty for ~$1B (Jan 2026)

Revenue: ~$200M (16 months)

Multiple: ~5x revenue, ~15x EBITDA

Dr. Squatch:

Acquired by Unilever for ~$1.5B (Feb 2026)

Revenue: ~$300M

Multiple: ~5x revenue

Why prestige beauty commands premium:

1. Higher gross margins:

Mass beauty: 50-60% gross margin

Prestige beauty: 70-80% gross margin

More profit per dollar of revenue

2. Brand equity:

Prestige brands have pricing power

Can raise prices 5-10% annually without losing customers

Inflation-resistant

3. Lower CAC:

Prestige beauty sells through Sephora, Ulta (retailer drives traffic)

Mass beauty relies on paid digital marketing

Prestige CAC: $20-40, Mass CAC: $50-80

4. Strategic value:

CPG giants (Unilever, P&G, Estée Lauder) need prestige brands to reach Gen Z

Willing to pay premium multiples for cultural relevance

Strategic buyers > financial buyers

VC takeaway: Prestige beauty exits at 15x EBITDA. Software exits at 8-12x EBITDA. Prestige beauty is more valuable than SaaS right now.

The New Rules: What’s Different From 2021

Consumer VC is back, but the playbook has completely changed.

Here’s what worked in 2021 vs. what works now:

Rule 1: Fewer Deals, Higher Conviction

2021 playbook:

Spray and pray (invest in 30-50 companies per fund)

Seed checks: $500K-1M

Hope 1-2 become unicorns

Portfolio construction: quantity over quality

2026 playbook:

Concentrated bets (invest in 15-20 companies per fund)

Seed checks: $1-3M

Expect $1-3M revenue before Series A

Timelines stretched: 3 years to Series A (vs. 18 months in 2021)

Why this matters:

In 2021: Founders could raise on pitch deck + prototype

In 2026: Founders need $1-3M revenue + retail traction + proof of retention

Capital efficiency is the new growth-at-all-costs.

What VCs are saying (from uploaded data):

“Seed investors now expect $1-3M revenue and retail traction; timelines to Series A have stretched to 3 years. Capital efficiency is key.”

Translation: If you’re raising seed in 2026, you better have 12-18 months of revenue data showing:

Product-market fit (repeat rate 40%+)

Unit economics work (LTV/CAC 3x+)

Path to profitability (not just growth)

2021 was about potential. 2026 is about proof.

Rule 2: Specialists Over Generalists

2021: Platform VCs (Forerunner, First Round, a16z) dominated consumer

2026: Specialist funds with category expertise are winning

The shift (from uploaded data):

“Platform VCs have moved on to AI. Active consumer investors now are specialist funds with focused strategies.”

What this means:

Generalist VC (2021):

Invested across consumer categories

Value-add: Brand building, DTC growth, fundraising intros

Thesis: Consumer brands are all similar

Specialist VC (2026):

Deep expertise in ONE category (beauty, beverage, food, wellness)

Value-add: Retailer intros, supply chain optimization, M&A positioning

Thesis: Every category has different unit economics and requires different playbooks

Examples of specialist funds:

Beauty-focused:

Prelude Growth (beauty + wellness only)

VMG Partners (CPG + beauty)

Beverage-focused:

CAVU (food + beverage, Poppi investor)

Wellness-focused:

Coefficient Capital + Apex ($530M, wellness tech)

Why specialists win:

Retailers trust them:

When VMG backs a beverage brand, Whole Foods pays attention

When Prelude backs a beauty brand, Sephora takes meetings

Specialist backing = retail credibility

They know unit economics:

Beauty: 70% GM, 15% marketing, 20% EBITDA target

Beverage: 60% GM, 20% marketing, 15% EBITDA target

Can spot bad deals faster

They have exit relationships:

Prelude knows who at Unilever buys beauty brands

CAVU knows who at PepsiCo buys beverage brands

Exit optionality built into investment thesis

If you’re raising consumer VC in 2026, target specialists first, generalists second.

Rule 3: $16B Is Deploying, But It’s Not Deployed Yet

The critical caveat (from uploaded data):

“~$16B is deploying right now. The next 12 months will test if this is a real recovery. Consumer VC remains small (3-6% of total VC), but specialists are showing strong signals.”

What this means:

$16B in fresh commitments ≠ $16B already invested.

Fresh commitments = LPs committed capital to funds, but funds haven’t deployed yet

Typical deployment timeline:

Year 1: 20-30% deployed

Year 2: 30-40% deployed

Year 3: 20-30% deployed

Year 4-5: Final 10-20% deployed

So of the $16B committed:

2026: $3-5B will actually deploy into companies

2027-2028: $8-10B deploys

2029-2030: Final $2-3B deploys

The test:

If brands funded in 2026 succeed (reach profitability, strong unit economics, exits at good multiples):

LPs will commit more capital to consumer VCs in 2027-2028

Virtuous cycle begins

If brands funded in 2026 struggle (burn cash, can’t reach profitability, no exits):

LPs will pull back again

We’re back to 2022-2024 drought

The next 12 months determine if this recovery is real or a false start.

The M&A That’s Validating the Model

Here’s why VCs are confident: $10B+ in consumer brand exits since Jan 2024 are proving the model works.

Major exits (Jan 2024 - Mar 2026):

$1.95B: Poppi → PepsiCo

Revenue: ~$400M

Multiple: ~4.9x revenue

CAVU return: ~88x (estimated)

~$1.5B: Dr. Squatch → Unilever

Revenue: ~$300M

Multiple: ~5x revenue

Category: Men’s personal care

~$1.2B: Siete Foods → PepsiCo

Revenue: ~$300M

Multiple: ~4x revenue

Category: Better-for-you Mexican food

~$1B: Rhode → e.l.f. Beauty

Revenue: ~$200M (16 months post-launch)

Multiple: ~5x revenue

Return for investors: TBD, but likely 10-20x

$880M: Touchland → Church & Dwight

Revenue: ~$100M

Multiple: ~8.8x revenue

Category: Premium hand sanitizer

$795M: Simple Mills → Flowers Foods

Revenue: ~$200M

Multiple: ~4x revenue

Category: Better-for-you snacking

Plus: LesserEvil (~$750M to Hershey), Bachan’s ($400M), TRUBAR ($173M), Four Roses ($775M)

Total consumer M&A (2024-2026): $10B+

Why this matters:

For every Poppi exit at 88x return:

That fund can return 3-5x to LPs on one deal alone

LPs reinvest in next fund

For every Rhode exit at 5x revenue in 16 months:

Proves celebrity + operator partnerships work

More VCs back celebrity brands

For every Dr. Squatch / Siete / Simple Mills exit:

Validates better-for-you positioning

More capital flows to similar brands

M&A exits create VC returns. VC returns attract LP capital. LP capital creates more M&A.

The flywheel is spinning again.

What This Means for Founders Building in 2026

If you’re building a consumer brand right now, here’s how to think about the current environment:

For Pre-Seed / Seed Founders:

Good news:

$16B in fresh capital means more shots on goal

Specialist funds understand your category better than generalists did

Capital is available if you have traction

Bad news:

Bar to raise is higher (need $1-3M revenue for Series A, not $500K)

Timeline stretched (3 years to Series A vs. 18 months in 2021)

You need to be profitable or near-profitable to raise growth rounds

What to optimize for:

1. Capital efficiency from day one:

Bootstrap to $1M revenue if possible

Raise small seed ($1-2M) to get to $3M revenue

Don’t raise big rounds until unit economics are bulletproof

2. Retail traction early:

VCs want proof you can get into Whole Foods, Target, Sephora

DTC-only brands are much harder to fund

Get into 100-500 doors before raising Series A

3. Category selection:

Functional beverages, GLP-1 nutrition, prestige beauty, wellness tech = hot

Traditional CPG, mass beauty, commoditized categories = cold

Pick categories where VCs are actively deploying

For Series A+ Founders:

Good news:

$1B+ funds (VMG, Forerunner, Prelude) are writing $10-30M checks

M&A multiples are healthy (4-5x revenue for growth brands)

Exit environment is strong

Bad news:

Expectations are higher (need 40%+ growth, 15-20% EBITDA)

Profitability required (can’t burn $10M/year anymore)

If you’re not on path to $100M+ revenue, tough to raise

What to optimize for:

1. Position for strategic acquisition:

Know which corporates buy in your category (Unilever for personal care, PepsiCo for beverages, etc.)

Build relationships early

Start M&A conversations at $50M revenue, not $200M

2. Build for platform, not point solution:

Poppi isn’t “one soda flavor” → it’s prebiotic soda platform

Rhode isn’t “one lip product” → it’s prestige skincare for Gen Z

Platforms exit at higher multiples than single products

3. Profitability > growth:

30% growth at 15% EBITDA > 100% growth at -30% EBITDA

VCs want to see you can scale profitably

Prove path to 20%+ EBITDA margins before Series B

For Later-Stage Founders ($50M+ Revenue):

Good news:

L Catterton has $11B to deploy into brands like yours

M&A buyers are active (Unilever, PepsiCo, Church & Dwight all acquiring)

This is your exit window

Bad news:

If you’re not growing 20%+ and profitable, you won’t exit at premium

IPO market still closed for consumer (only tech IPOs working)

Strategic acquisition is only exit path

What to optimize for:

1. Clean up cap table:

Too many small investors = messy M&A process

Consolidate if possible

Acquirers want clean deals

2. Professionalize operations:

Get real CFO, real finance systems, real audit

Acquirers will do deep diligence

Any accounting issues will crater valuation

3. Build strategic relationships now:

If Unilever might acquire you, start conversations 18 months before you want to sell

Let them get to know business, build trust

Best M&A deals happen through relationships, not auctions

The Final Reality

Consumer VC just had its best quarter since 2021.

$16 billion in fresh capital deploying.

Six major funds closed in 90 days.

$10B+ in M&A exits validating the model.

But this isn’t 2021 coming back:

2021 was:

Platform VCs investing everywhere

DTC brands raising on decks

Growth-at-all-costs

18-month timelines to Series A

Valuations at 20x revenue

2026 is:

Specialist VCs with category expertise

Brands raising on $1-3M revenue + retail traction

Capital efficiency required

3-year timelines to Series A

Valuations at 4-6x revenue (for profitable, growing brands)

The categories that are working:

Functional beverages (Poppi, Olipop)

GLP-1 nutrition (23% of households have GLP-1 user)

Wellness tech with SaaS economics (Oura at $11B valuation)

Prestige beauty (14.9x EBITDA multiples)

The categories that aren’t:

Traditional CPG (commoditized, low margins)

DTC-only brands (no retail path)

Mass beauty (9.8x EBITDA, half of prestige multiples)

The test:

The next 12 months will determine if this is a real recovery or another false start.

If brands funded in 2026:

Reach profitability (not just growth)

Build sustainable unit economics (LTV/CAC 5x+)

Exit at good multiples (4-5x revenue)

Then LPs will commit more capital, and the virtuous cycle continues.

If brands funded in 2026:

Burn cash without path to profitability

Struggle with unit economics

Can’t find exit buyers

Then we’re back to 2022-2024 drought.

Consumer VC is back. But it’s not the same game.

Build for capital efficiency. Build for specialists. Build for exit.

That’s the new playbook.

P.S. The smartest move I’m seeing from founders right now: Bootstrap to $1M revenue, then raise a small seed ($1-2M) to get to $3M revenue with retail traction, then raise Series A ($10-15M) from specialist fund with category expertise and retailer relationships. Total dilution: 25-35% vs. 50-70% in the 2021 playbook. You own more of your company at exit, and you have a specialist investor who can actually help you navigate retail and M&A. That’s how you win in 2026.